Finance

PrimeHedge.co review examines online trading education

PrimeHedge.co review examines trading education and course features

This PrimeHedge.co review explores the platform’s primary services, including trading education, personalized mentoring, market analysis, and support offerings. Global retail trading activity has surged in recent years and it highlights the rising demand for accessible and guided financial education platforms.

Primehedge is an online platform offering educational services designed to help individuals understand and participate in global financial markets. With over ten course options, the firm caters to traders at different experience levels.

PrimeHedge.co Review: What Does the Advanced Trading Course Offer?

In this PrimeHedge.co review, the accredited 12-week advanced trading course is featured as a structured program that provides professional-level training. Participants receive a level 5 diploma in applied financial trading upon completion. Many studies have proved that certified trading education can contribute to greater confidence and better decision-making among traders.

- Structured timeline: The course spans 12 weeks and progresses through multiple modules covering market theory, trading psychology, technical analysis, and strategy implementation.

- Professional accreditation: Participants get a level 5 certificate in applied financial trading upon completion, demonstrating knowledge and abilities relevant to trading positions.

- Mentorship access: During the course of the program, students collaborate with trade mentors who help them navigate real-world market situations and evaluate their own performance

What Does the Course on Financial Markets and Trading Cover?

The one-week financial markets and trading course, which provides an introduction to the trading environment for those who are unfamiliar with it, is also covered in this PrimeHedge.co review.

- Basic concepts: To get students ready for further education, the course covers market structure, asset kinds, trading platforms, and popular terminology.

- Short duration: Because it is intended to be finished in a week, anyone looking for a basic grasp without a long-term commitment can take it.

- Ideal for beginners: The framework facilitates novices’ getting acquainted with financial products and how they function in international markets.

How Does the Trading Analysis Service Work?

Trading analysis is a personal service offered to review past trades with professional guidance. This helps learners identify errors and adjust future strategies.

- Execution review: Participants submit executed trades for a detailed examination to uncover areas of poor judgment or missed opportunities.

- Feedback from mentors: Instructors provide direct commentary on trade timing, entry and exit points, and risk exposure.

- Customized improvements: The analysis leads to actionable changes in strategy, helping learners build more consistent approaches to trading.

What Kind of Valuable Advice Is Provided?

In this PrimeHedge.co review, the valuable advice service is a personalized course where learners receive practical insights from trading experts.

- Question-based sessions: Participants engage in Q&A discussions with experienced traders who address specific concerns or scenarios.

- Common mistake identification: Mentors explain recurring errors found among traders, helping participants avoid them in the future.

- Situational strategies: Based on each person’s trading background, objectives, and difficulties, tailored advice is given.

What Takes Place in a Comprehensive Debriefing?

The in-depth debriefing service is highlighted in this PrimeHedge.co review as an interactive, one-on-one training that focuses on real-time trading.

- Live trade explanation: A professional trader executes trades while explaining decisions step by step, giving insight into strategy and timing.

- Individual attention: Each session is tailored to the learner’s skill level and trading goals.

- Practical application: Real market conditions are used to teach decision-making, offering immediate exposure to the logic behind each move.

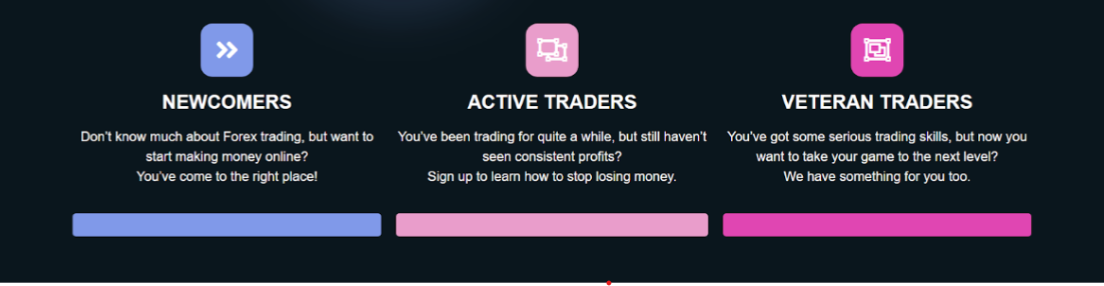

Who Are These Courses For?

Primehedge offers course options that align with the experience and goals of a wide range of individuals.

- Newcomers: Those unfamiliar with forex or trading can begin with introductory courses to understand basic principles and market behavior.

- Active traders: Individuals with trading experience but lacking consistent results may benefit from analytical reviews and mentoring.

- Veteran traders: Skilled professionals looking to refine strategies or enhance profitability can explore the advanced diploma and personal coaching options.

The OECD’s International Survey of Adult Financial Literacy Competencies highlights the global gap in financial education, emphasizing the need for structured learning programs for new market participants.

How Does the Registration Process Work?

In this PrimeHedge.co review, the platform is shown to offer a seamless registration process that enables users to begin their learning journey with minimal delay.

- Step-by-step form completion: Users provide basic personal information, select a course, and create login credentials.

- Flexible start dates: Many programs allow participants to choose a preferred start time that fits their schedule.

- Account verification: Registration includes account verification to ensure secure access to learning resources.

What Kind of Customer Support Is Available?

This PrimeHedge.co review outlines the contact options available for customer support. Assistance is provided through multiple channels.

- Phone numbers: Users can reach the support team at +442045711973 (UK) or +61285280927 (Australia).

- Email contact: Questions can be sent to support@primehedge.co for written assistance.

- Service accessibility: Support is available for both technical issues and course-related inquiries.

PrimeHedge.co Review on ScamAdviser

A reviewer shared that the 12-week advanced trading course surpassed expectations. It offered structure, access to mentors, and hands-on trading examples. The program helped the user develop confidence and practical knowledge, resulting in readiness to trade independently. The availability of such structured content without cost was seen as valuable.

PrimeHedge.co Review: Concluding Remarks

In this PrimeHedge.co review, the platform is presented as an educational hub with a diverse selection of trading-related courses and services. Programs are structured to accommodate learners from different backgrounds, offering professional accreditation, real-time mentorship, and targeted feedback. With its variety of course options and accessible customer support, the platform is positioned to help individuals progress in their trading education.

FAQs

How much time does it take to finish the course on advanced trading?

The 12-week advanced course culminates in a Level 5 diploma in applied financial trading.

Are these courses suitable for someone new to trading?

Yes. The financial markets and trading course offers an introductory program suitable for beginners, while other courses can be explored as the learner progresses.

How can someone register for Primehedge courses?

Interested individuals can sign up through the Primehedge website, verify their identity, and choose a course that fits their trading goals.

Is customer support available outside regular business hours?

Support can be reached via phone or email, but availability may vary depending on location and time zones.

Disclaimer: This article is intended solely for informational purposes and should not be considered as a recommendation. The author accepts no responsibility for any actions taken by the company during your trading experience. The information provided may not be fully accurate or current. Your trading and financial decisions are your own responsibility, and it is crucial not to rely solely on the content provided here. We make no guarantees about the accuracy of the information on this website and disclaim any liability for losses or damages resulting from trading or investing.

Investing feels like a huge step for many people. It is not just about picking a stock and hoping for the best. You need a map to reach your destination. If you start without a goal, you might end up in the wrong place. Many investors lose money as they do not have a clear plan. Setting your sights on a specific outcome makes every decision easier. This guide helps you find the right path for your money.

Define Your Financial Destination

Every journey starts with a target. You might want to buy a house in 5 years or retire in 30 years. One investment firm noted that turning these dreams into a plan is the first step to success. A short-term goal needs a different strategy than a long-term one. If you need cash soon, you cannot risk a market drop. Long-term goals let you ride out the bumps.

Consider these common targets for your money:

- Saving for a first-home deposit.

- Building a fund for your children’s school.

- Creating a steady income for retirement.

- Planning a major overseas trip.

Balancing Risk and Growth

Risk is a natural part of growing your wealth. Many investors rely on Opes Partners investment advice to help guide their financial decisions and build a portfolio that matches their goals. This choice dictates where your money goes. Some people prefer steady bonds – others like the fast pace of stocks. Your age and income play a big role in this choice. You should feel comfortable with the swings in your account value. If you lose sleep over a small drop, you may need a safer mix.

Building Your Safety Net

You cannot build a house on a shaky foundation. It is wise to have some cash set aside for unexpected costs. A recent guide suggests keeping a buffer of 5 to 10% of your income for emergencies. This includes things like car repairs or medical bills. This cash keeps you from selling your investments at a loss.

Debt is another factor to watch. High interest rates on credit cards can wipe out your gains. Data from a financial group shows that credit card interest rates now average 24.2%. Paying off debt is often the best first investment you can make. It gives you a guaranteed return by saving you from those high fees.

Planning for Every Life Stage

Your needs change as you get older. A young worker can afford to be aggressive. Someone nearing retirement needs to protect what they have. A retirement study mentions that 45-year-olds should have 3 times their salary saved. This metric helps you track if you are on the right path.

Mid-Life Adjustments

Every decade requires a new look at your strategy. If you are behind, you may need to save more or work longer. Life events like marriage or a new baby change your focus. You should check your progress at least once a year.

Understanding Market Value

The price you pay for an asset matters. Markets go through cycles of being cheap and expensive. A global strategy report found that the price-to-earnings ratio for global stocks recently hit a post-pandemic high of 18.3. This means stocks are currently pricier than they have been in years.

You should look at these numbers before putting all your cash into the market. Buying when prices are high can lead to lower returns later. Patience is often a winning strategy. It is better to wait for a fair price than to rush into a peak.

Managing Your Wealth and Taxes

Growing your money is only half the battle. You must keep it, too. Taxes can take a big bite out of your profits if you are not careful. A private bank suggests using tax-efficient ways to give money to family. For example, the annual gift limit is currently $19,000 per person.

This helps move wealth without losing it to the government. You should look at how different accounts are taxed. Choosing the right bucket for your money saves thousands over time. Small changes in how you hold assets make a huge difference in the long run.

Trends in Business and Interest Rates

Business activity tells us a lot about the future. Companies invest when they expect growth. A recent survey found that 86% of firms in Europe still plan to spend on new projects in 2025. This shows a level of confidence in the economy. It suggests that businesses see value in the years ahead.

Interest rates are moving in different directions around the world. A bank report indicates that yields on government bills are falling from 3% down to about 1.35%. Lower rates mean you might get less from your bank account. You may need to look at other options to get the return you want. Keep an eye on these trends to stay ahead of the curve.

Choosing the right path for your money takes time and thought. It is a process of learning what works for your life. You do not need to be a genius to see results. Just stay consistent and keep your eyes on the goal. Small steps lead to big changes over many years. Start today by looking at your current habits. Your future self will be glad you took the time to plan.

Money plays a significant role in everyday life, yet many people struggle to feel fully aware of their finances. Spending, saving, and borrowing can happen quickly and automatically, making it difficult to step back and see the whole picture. When financial activity feels unclear, it’s easy to feel uncertain or overwhelmed.

Personal finance apps are changing this experience by providing clearer insight into daily money habits. They help users track spending, monitor savings goals, and make informed decisions, turning what once felt like a blur of transactions into a more understandable and manageable picture. By keeping financial activity visible and organized, these tools make it easier for people to stay engaged with their money and approach financial decisions with confidence.

Teaching Money Skills Without a Classroom

Personal finance apps help people learn about money by connecting information to everyday activities. Instead of reading long explanations, users learn as they track their spending, saving, and borrowing. Seeing everything in one place makes money feel easier to understand.

Loans are one area where this kind of learning really shows up. For example, when people want to understand what is a cash loan, seeing how borrowed money appears alongside their other finances helps put the concept into perspective. This everyday exposure makes borrowing feel less abstract and supports more thoughtful money decisions.

Making Invisible Spending Visible

Many spending habits happen quietly and are easy to overlook. By analyzing income and spending patterns, financial tools can estimate future cash flow and flag potential issues before they happen. This helps people catch shortfalls or overspending in advance.

Personal finance apps make these details visible by organizing transactions in one place. When spending is clearly listed and grouped, patterns begin to stand out. This clarity helps people recognize habits they may not have noticed before. Once spending becomes visible, it becomes easier to make intentional choices. People can decide what feels necessary and what might need adjustment. This gives users greater control.

Turning Money Into a Daily Conversation

Personal finance apps have made it easier for people to stay on top of their finances regularly. Instead of waiting until a bill is due or a balance feels low, users can see updates as part of their daily routine. This frequent interaction helps money feel less intimidating and more familiar.

When money becomes part of everyday life, awareness naturally increases. People start noticing patterns in how they spend, save, and borrow without needing to sit down for long planning sessions. Small, consistent check-ins can be more effective than occasional deep dives.

Over time, this daily awareness changes how people think about their finances. Money shifts from something to avoid into something to understand. Users feel more informed and confident as financial activity becomes an everyday conversation.

Encouraging Goal-Driven Financial Decisions

Personal finance apps help people think about money with a purpose in mind. Instead of focusing only on day-to-day transactions, users are encouraged to look ahead and consider what they want their money to support. This shift helps turn financial decisions into meaningful steps.

When goals are visible, choices become clearer. Seeing progress toward saving, paying down balances, or planning makes it easier to stay focused. Even small advances can feel motivating when they are connected to a clear objective.

This goal-driven approach changes how people relate to money. Decisions are guided by intention rather than impulse. Over time, this mindset fosters greater financial awareness and more confident financial habits.

Reducing Money Anxiety Through Predictability

Uncertainty is one of the most significant sources of money stress. Uncertainty about upcoming expenses or available funds can create constant stress. Personal finance apps ease this worry by making financial information more transparent and easier to manage.

These tools organize financial activity to help people see what’s coming next. Viewing upcoming payments and recent trends helps users feel more prepared. Predictability creates a sense of stability, even when finances are tight.

With greater clarity, financial decisions feel less overwhelming. People can plan rather than react at the last minute. This shift from uncertainty to predictability plays a key role in improving overall money awareness and peace of mind.

Redefining What Financial Success Looks Like

Personal finance apps are helping shift how people define financial success. Instead of focusing only on perfect budgets or specific numbers, success is increasingly seen as understanding and control. Being aware of where money goes and why decisions are made has become just as important as the outcomes themselves.

This new perspective encourages progress over perfection. Minor improvements, consistency, and clarity now play a larger role in how people measure financial well-being. Personal finance apps support this mindset by promoting awareness and helping users make more intentional choices about their money.

The Impact of Greater Money Awareness

Greater awareness of personal finances can change how people feel about money. When financial information is clearer, everyday decisions feel more manageable and less stressful.

Personal finance apps play a role in this shift by helping people stay informed and engaged with their money. Over time, this awareness supports better habits and more thoughtful choices. A clearer understanding of money makes it easier to move forward with confidence.

When we think about planning for the future, our minds almost automatically drift toward numbers. We think about salary figures, savings goals, investment returns, and retirement nest eggs. The prevailing wisdom suggests that if you can just secure a high enough income, everything else will fall into place. Money, after all, provides options.

The Pitfalls of Chasing Income Without Clarity

Society often treats income as a scorecard. We are taught to climb the ladder, negotiate for more, and side-hustle our way to a higher tax bracket. While increasing your earning potential is a valid and often necessary goal, chasing it without a defined purpose can lead to a phenomenon known as “lifestyle creep.”

When income rises without a clear plan for those extra dollars, expenses tend to rise to meet them. You get a raise, so you buy a slightly nicer car. You get a bonus, so you book a slightly more expensive vacation. Before long, you are earning significantly more than you were five years ago, but your savings rate hasn’t budged. You are running on a faster treadmill, but you haven’t actually moved forward.

Furthermore, the pursuit of high income often comes with high costs—stress, long hours, and time away from family. If you don’t have clarity on why you are making those sacrifices, resentment builds. You might wake up twenty years from now with a healthy bank balance but a life that feels empty because you spent decades funding a lifestyle you didn’t actually value.

How Clarity Leads to Better Financial Decisions

Clarity acts as a filter. When you know exactly what you want your life to look like—in five years, ten years, or during retirement—spending and saving decisions become significantly easier.

Imagine two people:

- Person Awants to retire early at 50 to travel the world in a van.

- Person Bloves their career and wants to work until 70, but wants to buy a large farmhouse for their extended family to visit.

These two distinct visions require completely different financial strategies.

- Person A needs to prioritize an aggressive savings rate now, perhaps sacrificing luxury housing and new cars to build a freedom fund.

- Person B might be comfortable saving less aggressively now, but needs to focus on real estate investments and long-term career stability.

When you have this level of clarity, you stop spending money on things that don’t align with your goals. You stop trying to keep up with the Joneses because you realize the Joneses are playing a different game than you are. Clarity transforms budgeting from a restrictive chore into a strategic tool for getting what you actually want. It turns “I can’t afford that” into “I choose not to spend on that because I prefer this.”

Practical Steps to Gain Clarity in Your Life

Finding clarity isn’t always a lightning-bolt moment; it’s usually a process of excavation. You have to dig through societal expectations and other people’s opinions to find your own values. Here are a few ways to start:

1. The “Perfect Day” Exercise

Close your eyes and visualize your perfect average Tuesday five years from now. Where do you wake up? Who is with you? What work are you doing? How do you spend your evening? Be specific. This visualization often reveals what you value most—whether it’s autonomy, community, creativity, or stability.

2. Audit Your Spending vs. Your Values

Look at your last three months of bank statements. Highlight the top three categories where your money went (excluding fixed costs like rent/mortgage). Do those categories align with what you say is important to you? If you say you value travel but spend 20% of your income on dining out locally, there is a misalignment.

3. Seek Professional Guidance

Sometimes, we are too close to our own lives to see the patterns. This is where professional help shines. Consulting a finance planning and wealth management advisor in St. George isn’t just about picking stocks or minimizing taxes. A good advisor acts as a mirror, reflecting your values to you and showing you how your current financial behavior aids or hinders your true goals. They can ask the hard questions that force you to define what “enough” looks like for you.

Conclusion

It is easy to measure income. It fits neatly into spreadsheets and graphs. Clarity is harder to quantify, which is why it is often overlooked. But ultimately, money is just a tool. A hammer is useful if you are building a house, but it’s useless if you don’t have a blueprint.

-

Blog7 months ago

Blog7 months agohanime1: The Ultimate Destination for Anime Lovers

-

Entertainment9 months ago

Entertainment9 months agoSflix: How It’s Changing the Way We Watch Movies and TV Shows

-

Entertainment8 months ago

Entertainment8 months agoCrackstreams 2.0: The Future of Free Sports Streaming?

-

Bills10 months ago

Bills10 months agoWhy Does My Instagram Reel Stop Getting Views After One Hour? How to Fix It?

-

Technology10 months ago

Technology10 months agoSimpcitt: The Rise of a Unique Online Community

-

Blog8 months ago

Blog8 months agoImginn: The Ultimate Tool to View Instagram Content Anonymously

-

80s10 months ago

80s10 months agoFavorite 100 Songs of the 80s: (#1) Michael Jackson – Billie Jean

-

Blog10 months ago

Blog10 months agoSimpcitu: The New Age Trend Shaping Online Interactions